❑Understanding certain Accounting Terms and the various General Ledger associated Maintenance Entries and Reports:

•These are the key Terms and Reports that, if you understand them, will make starting and using this General Ledger System much easier:

1.Account Divisions (which are not related, and have nothing to do with Division(s) within your Company

a.There are several predefined types Account Divisions that may be assigned to a General Ledger Account

b.These Account Divisions classify the kinds of Financial Transactions that will be posted to the General Ledger Account , and so will properly characterize the Values (Balances) they hold (see the "Types of Account Divisions" discussion immediately below).

c.There are five Primary classifications of General Ledger Accounts: 1.) Assets, 2.) Liabilities, 3.) Equity, 4.) Sales, and 5.) Expenses.

d.Many of these Primary classifications often require that sub-classifications of Accounts also be included on most Financial Statements, and so they are also included in this General Ledger System as (Secondary) sub-classifications within the default set of Account Divisions

e.These Account Division classifications and sub-classifications will determine whether the General Ledger Account is a Debit or a Credit type of Account (see the Understanding Debits & Credits chapter for more information on these Terms).

f.Just as important, these classifications also determine where and when these Accounts will appear within the Balance Sheet and/or the Income Statement reports.

2.General Ledger Groups - These Groups are used to further sub-divide the Account Division classifications and sub-classifications (see #1, a. - c. above) into additional sub-groups (see #3 below, and the General Ledger Accounts and Account Groups chapters for more information).

3.General Ledger Accounts - This is the set of "Accounts" - each of which are created with an Account Name (referred to as its Title), a Number (i.e., its Account Number), and are assigned to an Account Group (to which an Account Division has also been assigned)

a.The assigned Account Group identifies where - within their assigned Account Division - those Accounts will appear within the Balance Sheet and/or the Income Statement.

b.These Accounts will contain the net dollar amount posted to them (referred to as the Account's Balance) resulting from:

i.positive dollar Values entries (Debits posted to Debit Accounts and Credits posted to Credit Accounts); and

ii.negative dollar Values entries (Credits posted to Debit Accounts and Debits posted to Credit Accounts).

4.Trial Balance - This is the report that provides a comparison of the sum of all Debit and Credit Financial Transactions, posted to all of the Debit and Credit Accounts (see the Understanding Debits & Credits chapter for more information on these Terms), and so determines whether your Company's General Ledger is, or is not in balance.

5.Income Statement - This is the report that provides a comparison between the posted Sales and the posted Expenses, reporting the net difference (within a specified Date Range) as a Profit (if the Sales exceed the Expenses, or a Loss, if the Expenses were greater than the Sales).

6.Balance Sheet - This is the report that provides, on a month by month, or annualized basis, the value of the Company's Assets, Liabilities, and its net Equity position.

7.Cash Flow Statement - This provides a Statement of Cash Flows that reports the Description and net Amounts of the Operating, Financing, and Investing related Financial Transactions that increased and/or decreased the Value of your Company's Cash Position.

8.Transaction File - The Transaction File lists the Debit and Credit entries that were posted to any and all General Ledger Accounts within a specified Date Range.

9.General Journal - The General Journal Form provides the mechanism for manually inserting Financial Transaction entries directly into your General Ledger's Transaction File.

10.Account Register - The Account Register provides a set selection criteria to filter a list of the Debit and Credit entries that were posted to one specified General Ledger Account.

❑Types of Account Divisions

•There are several default Transaction Types - identified here as Account Divisions - that characterize the general Purpose and Functionality of the General Ledger Account to which it was assigned.

➢Note: A Company Division has a very different meaning and purpose then the term "Account Division" which is used here to specifically identify Transaction Types.

a)Divisions allow a Company to define and separate certain business related entities within their Company - typically for territorial reasons or for product line differentiation - into specific Company Divisions.

b)Account Divisions are used to specifically identify the Transaction Types discussed below.

•Each Account Division within your Company's General Ledger will automatically contain its associated set of General Ledger Accounts because:

1.Each General Ledger Account is assigned to a General Ledger Group

2.Each General Ledger Group is assigned to an Account Division

3.Therefore, each General Ledger Account is automatically associated with, and therefore identified as a member of an Account Division.

•General Ledger Account Numbers - based on their General Ledger Grouping and therefore their associated Account Division - should be assigned within a designated Account Numbering Range - and the Account Numbering scheme proposed below is the recommended method.

✓Because the Account Numbering Range described below is only our recommendation, your Company's Accountant might suggest a different numbering scheme.

✓General Ledger Account Numbers may contain up to 8 digits; plus 4 additional digits coming after a decimal point (e.g., 12345678.1234)

▪Just because this capability is available, does not mean it should be used.

▪Simplicity in implementing an Account Numbering Range is always preferable.

▪The Account Numbering scheme that is proposed below will accommodate most businesses.

✓That said, any numbering scheme (designed within the parameters explained above - i.e., each General Ledger Account is assigned to an Account Group which has been assigned to an Account Division) may be implemented by your Company's Accountant and can be accommodated by this General Ledger System.

•The Type of the Account Division (i.e., Transaction Types) its recommended Account Numbering Range, and whether they represent a Debit or a Credit Account (see the "Understanding Debits & Credits" chapter for detailed information), are listed here:

1.Asset Accounts (the available predefined Account Divisions are: Assets - the Primary Account Division, plus the Secondary Account Divisions of Bank, Accounts Receivable, Other Current Assets, Fixed Assets, Other Assets): 1000 - 1999 - Debit - An Asset Account identifies items that have an actual cash value or can reasonably be converted to cash and are generally sub-divided into these categories:

a)Actual Cash Assets (like real money in a Petty Cash box, and the money in a Bank or Money Market account).

b)Current Assets (things of value that the Company owns or is entitled to) like monies other people or businesses owe your Company (Accounts Receivable)

c)Other Assets such as your Company's Furniture, Computers, Vehicles, Inventory and/or Real Estate.

1.Liability Accounts (the available predefined Account Divisions are: Liability - the Primary Account Division, plus the Secondary Account Divisions of Accounts Payable, Other Current Liability, Credit Card, Loan, Long Term Liability): 2000 - 2999 - Credit - Each Liability Account identifies some portion of what the Company owes, or in some other manner is obligated to pay to, or is owned by others.

a)Current Liabilities would include Short Term Liabilities such as the Accounts Payable balances owed to Vendors, Inventory Purchases (a temporary holding account for users of the Inventory Tracking System) and things like Payroll Taxes and Credit Card debt that generally must be paid within the current Fiscal Year.

b)Long Term Liabilities would be items such as amortized business loans and mortgages that are generally repaid over an extended period of years.

2.Equity Accounts (Available predefined Account Division is: Equity - the Primary Account Division (there are no predefined Secondary Account Divisions for Equity) 3000 - 3999 - Credit - Equity Accounts identify the net value of the business.

a)Start Up Capital records the original investment in the business and any additional Capital that may have been contributed to your Company afterwords.

b)Earnings which are the business's Current Earnings for this Fiscal Year.

c)Retained Earnings which are the business's Earnings - which represent Profits (or Losses) from previous years - and have not yet been paid out to Shareholders or Partners.

3.Sales Accounts (Available predefined Account Divisions are: Sales - the Primary Account Division, plus the Secondary Account Divisions of Income, Other Income): 4000 - 4999 - Credit - This identifies the Revenue from Sales, Interest earned from savings and other investments, and any other miscellaneous Income.

a)Sales which represent any income (Revenue of almost any type) that is earned by your Company in the normal course of business.

b)Other Income for any other type of income you might receive (Interest Earned, Dividends, abandoned Deposits, etc.)

4.Expense Accounts (Available predefined Account Divisions are: Expense - the Primary Account Division, plus the Secondary Account Divisions of Cost of Goods Sold, Other Expense): 5000 - 9999 - Debit - Purchases made to sustain the business, produce product, complete installations and/or provide services.

a)General Expenses including things like Rent, Utilities, Payroll, Health and other type of Insurance, Shipping, Postage, Office Supplies, Interest for Loans, and Taxes.

b)Cost of Goods Sold includes Inventory which has been used for business purposes, and any associated Adjustments (for "shrink" and/or breakage)

c)Sales related Expenses such as Commissions, Costs for Installations, Service related Expenses, etc.

d)Earnings Posting which is a Special Account used by the system (see the Mandatory Accounts chapter for more information)

✓Although your Company's General Ledger Account Numbering scheme (see the "Choosing the Account Numbering scheme" discussion immediately below) may contain up to 8 digits; plus 4 additional digits coming after a decimal point (e.g., 12345678.1234), the list below presents a typical - and our recommended - Account Numbering scheme (the recommended Numbering Range) for each of the five Primary Account Divisions:

▪Asset Accounts 1000 - 1999 - Debit - An Asset Account identifies items that have an actual cash value or can reasonably be converted to cash;

▪Liability Accounts 2000 - 2999 - Credit - A Liability Account identifies a portion of what the Company owes, or in some other manner is obligated to pay to, or is actually owned by, others;

▪Equity Accounts 3000 - 3999 - Credit - The Equity Accounts identify the net value of the business (Company) and ultimately equals the Company's Assets minus its Liabilities;

▪Sales Accounts 4000 - 4999 - Credit - These Revenue Accounts identify the Revenue (Income) from Sales, Interest earned from savings, and any other miscellaneous Income;

▪Expense Accounts 5000 - 9989 - Debit - These Expense Accounts identify the Purchases made to sustain the business, produce product, complete an installation, and/or provide services.

•Choosing the Account Numbering scheme - The Account Numbering scheme and the Numbering Range for each Primary Account Division that will be used for designing your Company's Chart of Accounts (i.e., the full set of General Ledger Accounts):

✓Although a Numbering Range of 1000 to 9999 is recommended, a much more complex numbering scheme may be utilized, if necessary:

▪Up to 9,999,999 main General Ledger Accounts, each with up to 9,999 subordinate Accounts may be created (e.g., 12345678.1234).

▪This power and capacity must be used wisely, because the longer and more complex the number scheme adopted for defining your Company's General Ledger Accounts becomes, the more complicated the management and reporting will be for this (or any) General Ledger System.

▪Remember: With Power comes Responsibility

✓So, unless you have a compelling reason to be more complicated and complex when designing your Numbering Range, stick with our recommendation (i.e., a Numbering Range of 1000 to 9999).

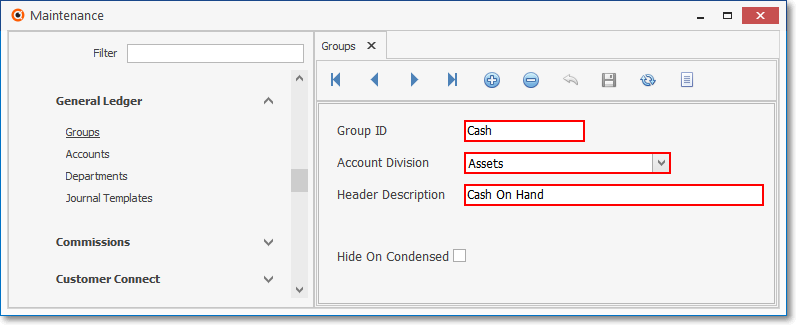

❑General Ledger Group IDs - General Ledger Groups are used to sub-divide the assigned Primary or Secondary Account Division (see the General Ledger Accounts and Account Divisions chapters for more information) into additional sub-group classifications.

•General Ledger Group names (Header Description) will appear as sub-headers - and are shown with their own individual sub-totals - when Financial Statements are printed or viewed.

✓Your Company's Groups must be defined before creating your Company's General Ledger Accounts because each General Ledger Account requires the assignment of a Group ID.

Maintenance Menu - General Ledger - Groups Form

✓A Footer for each sub-header (with the Header Description) will be inserted to the left of their associated sub-total.

✓The assignment of a Group ID to a specific General Ledger Account ensures that the Account will be grouped with, and will be included in the Footer's sub-total for that Group.

✓Within each Group, its associated Accounts will be listed in numerical order.

✓Optionally, using the Hide On Condensed reporting option, the inclusion of just the Name of the Group's Header Description and its sub-total Amount may be requested by the User when printed.

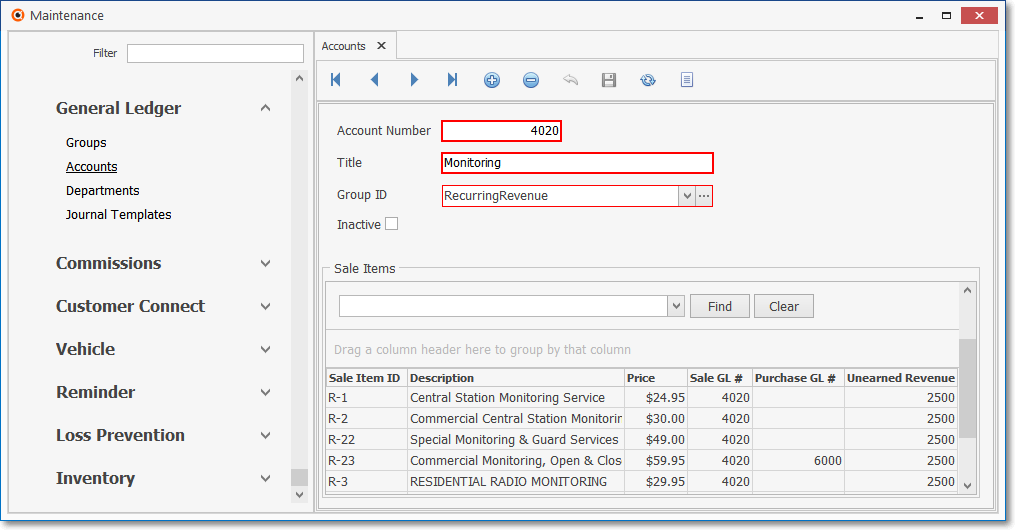

❑Chart of Accounts - A "Chart of Accounts" is actually a list of the General Ledger Accounts - presented in numerical order - which have been defined for a General Ledger System, and may include the current Balance of each Account for the most recently Closed Accounting Period as is typically presented on the Trial Balance report.

❑General Ledger Accounts - A "Chart of Accounts" is actually a list of the General Ledger Accounts which have been defined for this General Ledger System and may include the current Balance of each Account that existed in the most recently Closed Period.

•A list of the General Ledger Accounts (a.k.a. Chart of Accounts) is simply a list of those "Accounts" identified by an Account Name (its Title), and a Number (the assigned Account Number) which ultimately will "hold" the net sum total of the dollar values (referred to as the Account's Balance) which have been posted to them.

Maintenance Menu - General Ledger - Accounts Form

✓These General Ledger Accounts are separated within the Chart of Accounts by the Type of Transactions (their Account Division) which are posted to each of those Accounts (see #1 - #5 in the "Type of Account Division" section immediately above).

✓The General Ledger Accounts must be segmented further - within each Transaction Type listed in the Chart of Accounts - by having them assigned to a General Ledger Account Group.

✓All of this is done to enable the User to clearly understand the Purpose and Functionality of each General Ledger Account within their Chart of Accounts (see below).

❑Trial Balance report provides a view of the gross balance posted to all General Ledger Accounts.

•The Total Values posted to all of the Credit Accounts should equal the Total Values posted to all of the Debit Accounts.

•Because this Trial Balance Report provides a comparison of all of the Debit and Credit transaction entries, which have been posted to all of the Debit and Credit Accounts, it will report whether or not the General Ledger is currently "in balance".

❑Income Statement calculates the Net Profit (Loss) for a designated accounting period.

•It produces a list of the Revenue Accounts with a subtotal, followed by the Expense Accounts with a subtotal, and the net difference between them (if the Revenues are greater than the Expenses, there is a Profit, otherwise there is a Loss).

•This Income Statement is based on a Date Range (usually a selected month or year) and may be produced for a specific accounting period, for a specified Department, and with, or without Graphs or Charts.

❑Balance Sheet lists the balance of each Asset Account with a subtotal, then the balance of each Liability Account with a subtotal, and (what is actually) the net difference between them - which is the Company's (Stockholders') Equity.

•That difference is divided among the Equity Accounts based on why that Equity (e.g., derived from a Profit, Capital invested in the Company, Additional Paid in Capital, etc.) Account has been defined.

❑Cash Flow Statement - Calculates the Company's Net Cash Flow as of a specified Date

•The system calculates Net Cash Flow as follows:

a)Calculate the Operating Value (The Net Income from a selected Accounting Period + Change in Operating Activities from end of previous Accounting Period to end of current - selected - Accounting Period)

b)Then, subtract the Inventing Value (Change in Investing Activities from end of previous Accounting Period to the end of current Accounting Period)

c)Then, subtract the Financing Value (Change in Financing Activities from end of previous Accounting Period to end of current Accounting Period)

✓The result is the Net Cash Flow for the selected Accounting Period being reported.

❑General Journal provides a dialog to make special entries directly into the General Ledger without using the Accounts Receivable, Accounts Payable and/or Inventory Tracking & Job Costing modules.

•This feature, initially used to establish the General Ledger's starting balances, is most commonly used to post Payroll from an outside service (or separate software application) and is required for making special end-of-period entries (e.g., Depreciation, Previously Deferred Revenue which has been Earned, Inventory Valuation Adjustments, etc.) required by the Company's Accountant.

•Templates may be designed to improve the accuracy and speed of making repetitive General Journal entries.